Get the Money Moving to drive the climate transition

What’s needed for European corporates

to meet net-zero goals

Get the Money Moving to drive the climate transition

What’s needed for European corporates

to meet net-zero goals

-

-

-

-

Link copied

Link copied

Only one in five European companies is making the kind of substantive changes necessary to move to a greener business model, even as more than half report having climate transition plans in place. An even larger number has set emission-reduction targets, including a portion for Scope 3 supply chain and end user emissions.

This research in the 2024 CDP report "Get The Money Moving" is based on an analysis of responses from more than 1,600 European companies disclosing through CDP, representing 89% of the region’s market capitalization. It assesses companies against a five-point framework looking at critical factors such as capital investment, new product development, and supply chain management. While the data demonstrates progress by companies in reducing emissions over the last four years, it also reveals the substantial limits that still exist in implementing key aspects of transition plans and driving real change on business models.

Exhibit 1: Progress toward a Green Business Model

Distribution in percentages (%)

Source: Oliver Wyman analysis, CDP data

Exhibit 2: Utilities, steel, and transport lead on closing the implementation gap

Distribution in percentages (%)

Note: The implementation gap framework evaluates companies on five key drivers of a transition to a green business model: Steering the business, capital expenditure, supplier decarbonization efforts, engagement with customers, low carbon product, and technology innovation

Source: Oliver Wyman analysis, CDP data

Investment capital is key to green transition

Levels of capital investment play a critical role in whether a company can achieve results. Yet 70% of European companies disclosing through CDP dedicated less than a quarter of their capital expenditures (CapEx) to projects that are aligned with their transition plan or a sustainable finance taxonomy. In some cases, accessing finance is part of the challenge. One-third of companies disclosing through CDP identified access to capital as a key concern in transition planning. That percentage rose dramatically among industries with higher emissions.

Exhibit 3: Green Capital Expenditures varies widely across industries

Distribution in percentages (%)

Note: Question C3.5a – Quantify the percentage share of your spending/revenue that is aligned with your organization’s climate transition

Source: Oliver Wyman analysis, CDP data

Often the common constraint for companies and financial institutions is that green business models remain less commercially attractive than the existing models they seek to replace. In many sectors, government policy has not yet shifted the economic landscape decisively enough in favor of greener products and services. At the same time, in many industries, the demand for “green” products or the willingness to pay a premium for those is still limited. There is a concern that while Europe has led the way in many aspects of climate regulation and policy, other regions have taken bolder action using incentives and industrial policy to attract investment capital and build competitive advantages in strategically important parts of the green economy.

Sectors that could help focus on decarbonization

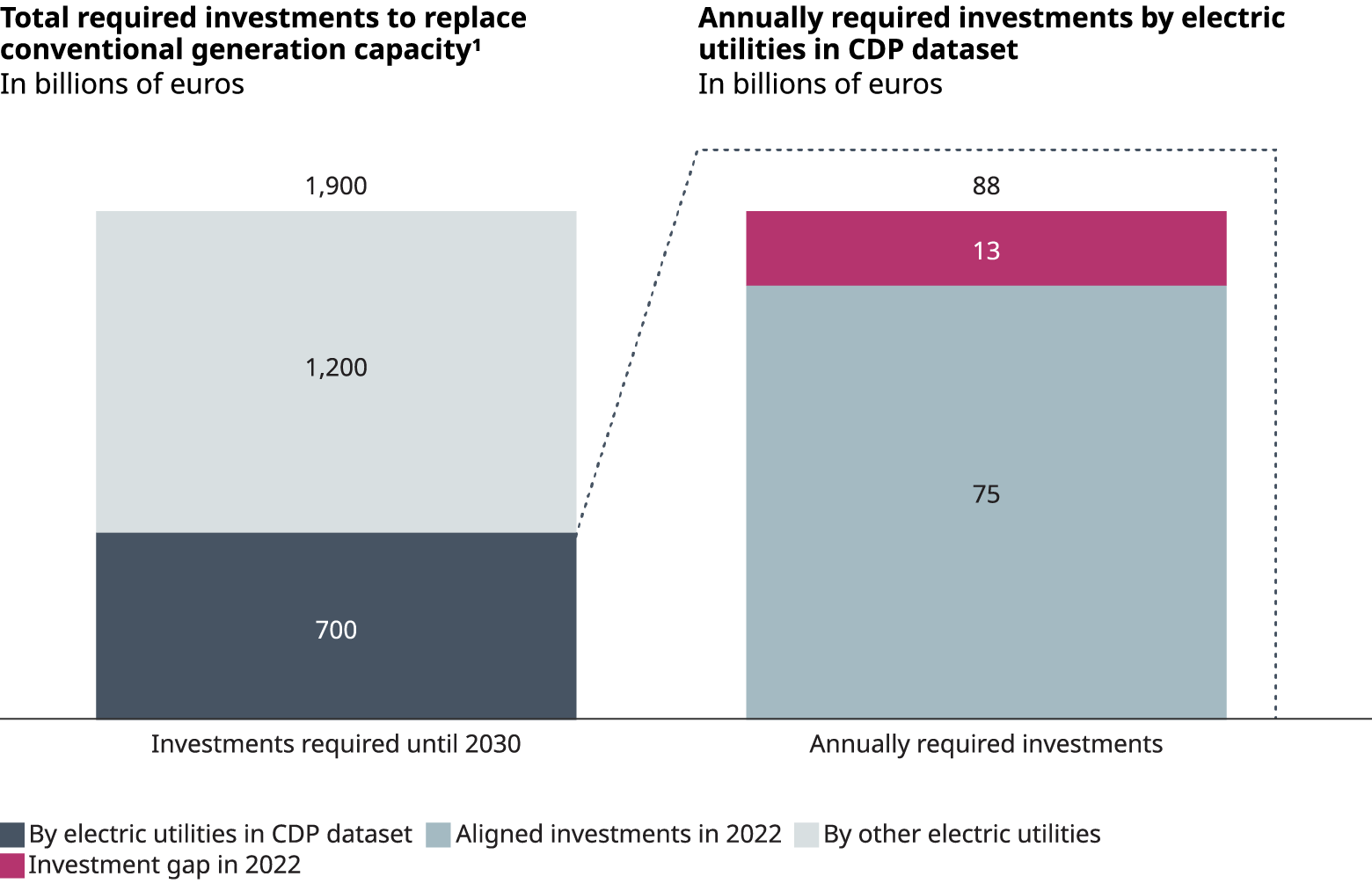

To explore the practical realities companies are facing, we looked in greater detail at three critical sectors: electric utilities, steel, and automotive. All three are major emitters and play a pivotal role in the decarbonization of many other sectors. The good news is that the three are already investing more than most in the transition — with over 50% of CapEx going to green initiatives. Still, some important gaps and disconnects are apparent:

- By 2030, electric utilities could fall €285 billion short on required CapEx investments in renewables and upgrading the grid key to the push to electrify and decarbonize transport and heavy industry.

Exhibit 4: Capital investment utilities need to make to achieve emissions reduction

Notes: 1. Including coal-and oil-based but not gas-based power generation capacity. 2. Total conventional power generation capacity in EU to be replaced = 230GW. 3. Including only electric utilities that generated conventional power in 2022 and grid operators

Source: Oliver Wyman analysis, CDP data, IEA data, Capital IQ data (23.11.2023), rounding errors may occur

- While 87% of steel companies offer some type of low-carbon products, revenue from green products accounts for only 22% of total sales. As a result, green steel production is expected to fall as much as 18 million metric tons, or 31%, short of demand by 2035.

Exhibit 5: Low carbon products represent a small share of revenue in most industries

Distribution in percentages (%)

Note: Question C4.5a – Provide details of your products and/or services that you classify as low-carbon products

Source: Oliver Wyman analysis, CDP data

Exhibit 6: Rising green steel demand creates shortage of 18 million metric tons by 2035

CBAM: Starting in 2026, imported grey steel into Europe will be subject to an extra tariff making grey imports more expensive and European green steel more attractive

Free allowance phase out: Starting in 2026, European steel producers will gradually lose their free allowances, which in turn raises grey steel prices further driving green steel demand

Base demand: Driven by the carbon reduction goals of the separate industries and their demand growth

Source: Oliver Wyman analysis

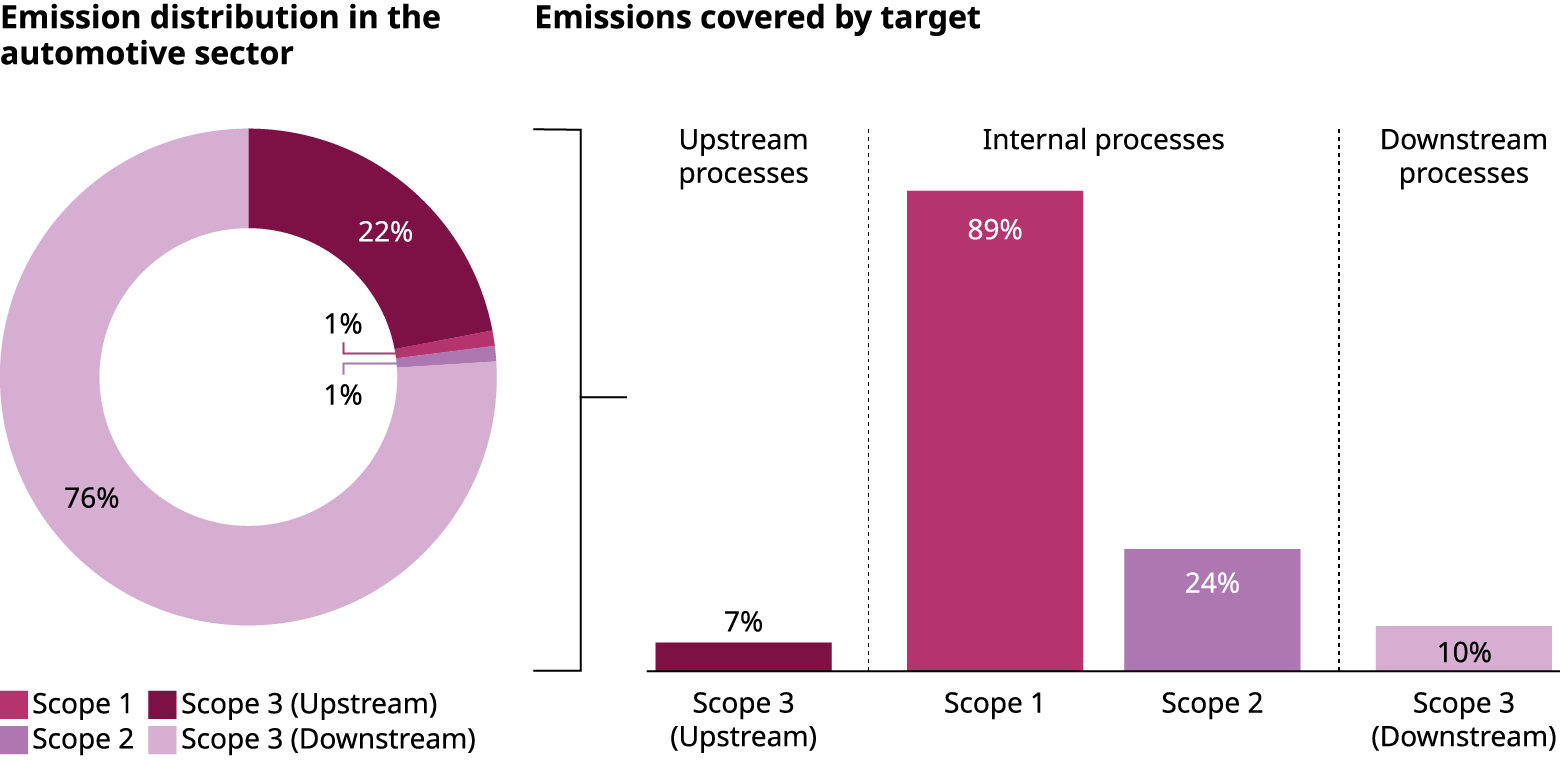

- The vast majority (90%) of the automotive industry’s carbon footprint is made up of Scope 3 emissions from its supply chain and end users. Yet only 11% of companies ensure that over 25% of their suppliers meet climate-related requirements.

Exhibit 7: Scope 3 emissions are automotive’s big hurdle, with little progress realized

Source: Oliver Wyman analysis, CDP data

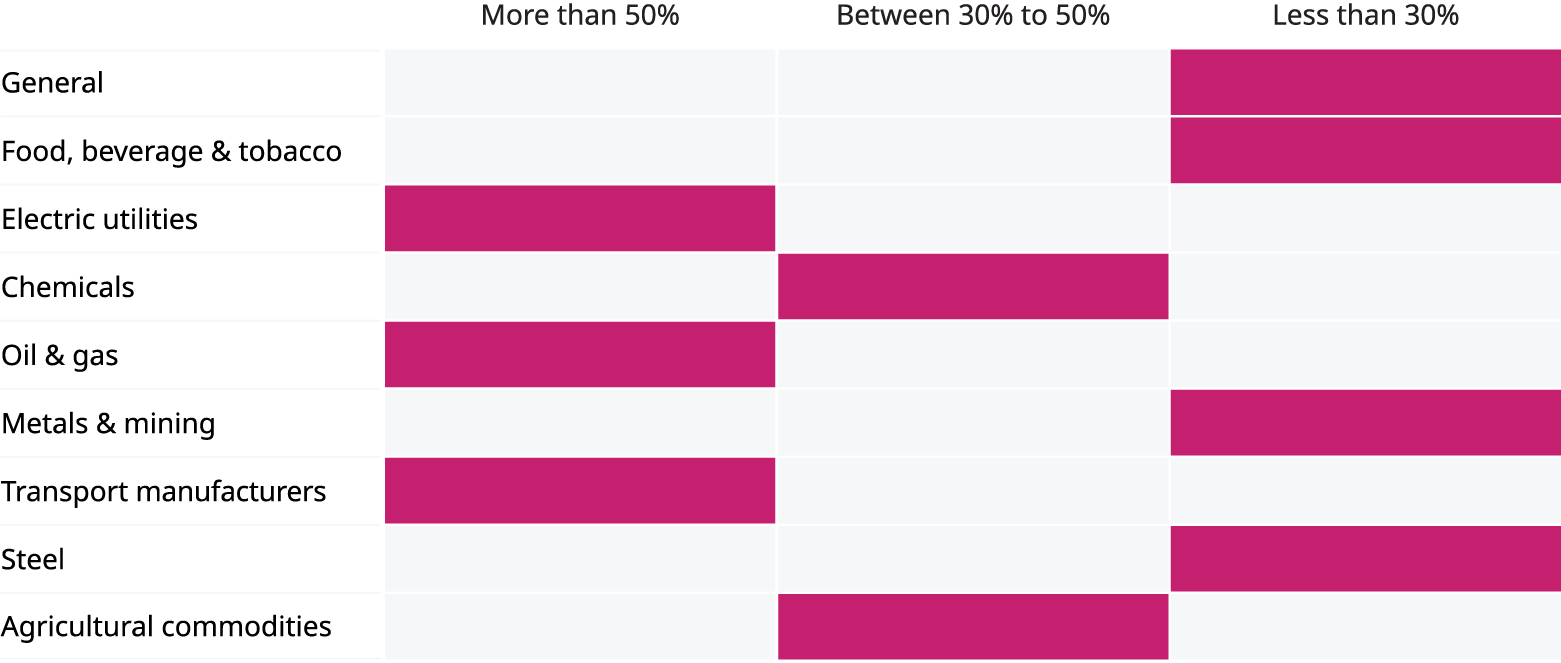

Exhibit 8: Few industries have made deep progress in purchasing contract requirements

Distribution in percentages (%)

Note: Question C12.2a – Provide details of the climate-related requirements that suppliers have to meet as part of your organization’s purchasing process and the compliance mechanisms in place

Source: Oliver Wyman analysis, CDP data

Freeing up more investment for green initiatives

The challenges companies highlighted in accessing capital come despite major commitments from the finance sector. Two-thirds of financial institutions disclosing through CDP say they are taking active steps to align their portfolios to an emissions pathway that curbs Earth’s temperature increase to 1.5°Celsius above pre-industrial levels.

Most are seeking to do this through growing investment and lending into greener areas: Financial institutions globally disclosed through CDP in 2022 that they view the potential opportunities from the climate transition as 4.5 times greater than the risks. Meanwhile, exclusion policies remain mostly limited to coal and the most environmentally sensitive parts of the oil and gas industry.

Exhibit 9: Most financial services companies are assessing whether the corporates they finance are aligned with 1.5 degrees

Number of companies and percentage (%) of companies

Source: Oliver Wyman analysis, CDP data

Most financial institutions report that they are now actively assessing their client’s transition plans as part of their lending and investing processes, suggesting that companies not able to set out a clear decarbonization path may find access to capital more challenging over time. In practice, however, it is the unique characteristics of decarbonization projects that can become hurdles. This includes their often-large-size, longer time horizons, unproven markets, misalignment with institutional risk appetites, and the changing regulatory landscape they face.

Exhibit 10: Many companies cite access to capital as a key concern

Companies identifying access to capital as key factor influencing their financial planning, distribution in percentages (%)

Notes: 1. Carbon Border Adjustment Mechanism (CBAM), 2. Inflation Reduction Act (IRA)

Source: Oliver Wyman analysis, CDP data

Exhibit 11: Pain points faced by corporates in accessing capital

Notes: Summary of key issues relate to disclosures to CDP on access to capital raised by corporates 1. Carbon Border Adjustment Mechanism (CBAM), 2. Inflation Reduction Act (IRA)

Source: Oliver Wyman analysis, CDP data

Nature's role in economy and climate

Efforts to prevent deforestation and protect water sources are the latest standards that are just beginning to take hold. Half of the world’s economy is dependent on nature, according to the World Economic Forum, which makes its salvation critical to more than just climate. Forests and bodies of water also serve as natural carbon sinks, and the outlook for climate change worsens without them.

But at this point, neither financial institutions nor industrial companies are routinely including concerns like deforestation and water security in their investment decisions or transition planning. The CDP disclosure data shows over 50% of financial institutions have no plans to protect water security or set targets for preventing further deforestation. Only 9% have set specific goals related to deforestation in their lending and investment activities, and 1% have targets for water security. This low participation may change with new European Union requirements on nature.

The need for collective action

The report encourages greater collaboration across the financial sector to spread risk among banks, development banks, private equity firms, insurance companies, traditional infrastructure financiers, and philanthropic organizations. It also calls on governments to take a more active role in leveling the playing field for climate transition products and technologies.

The data on both climate and nature reinforces the reality that no one industry can create a green transition without the support of the global economic community, governments, and nongovernmental organization. As time ticks off to 2030, the year the EU promises to cut emissions 55% as part of its 2050 net-zero pledge, the need to significantly accelerate efforts could not be clearer.

Exhibit 12: Heatmap: Disclosure against the five key elements of a transition plan

Percentage (%) of companies showing progress and comparison versus 2022

Note: 1. 2022 data set

Source: Oliver Wyman analysis, CDP data

Case studies

Featured case study

Beiersdorf

Sector – General

Featured case study

L’Oréal

Sector – General

Featured case study

MM Group

Sector – Paper and forestry

Featured case study

Symrise

Sector – Chemicals

Case study

E.ON

Sector – Electric utilities

Case study

La Banque Postale

Sector – Financial services

Case study

Lenzing

Sector – Chemicals

Case study

KBC

Sector – Financial services

Case study

Solvay

Sector – Chemicals

Case study

Stahl-Holding-Saar

Sector – Steel

Case study

Storebrand

Sector – Financial services

Case study

Zurich Insurance Group

Sector – Financial services